Janell A. Israel & Associates

1585 Kapiolani Blvd., Suite 1604, Honolulu, Hawaii 96814 Phone: 808-942-8817

May 2018 Tax Newsletter

Update on the Tax Cuts and Jobs Act (TCJA)

The Tax Cuts and Jobs Act (TCJA) was passed by Congress in a hurry late last year, and the IRS and tax preparers have been working to digest some of the more thorny issues created by the tax overhaul. Here are the latest answers to some of the most common questions:

- Is home equity interest still

deductible?

The short answer is: Not unless you’ve used the money to buy, build or substantially improve your home.

Before the TCJA, homeowners were able to take out a home equity loan and spend it on things other than their residence, such as to pay off credit card debt or to finance large consumer purchases. Under the old tax code, they could deduct interest on up to $100,000 of such home equity debt.

The TCJA effectively writes the concept of home equity indebtedness out of the tax code. Now you can only deduct interest on “acquisition indebtedness,” meaning a loan secured by a qualified residence that is used to buy, build or substantially improve it. If you have taken out a home equity loan before 2018 and used it for any other purpose, interest on it is no longer deductible.

- I'm a small business owner. How

do I use the new 20 percent qualified business expense deduction?

Short answer: It’s complicated and you should get help.

Certain small businesses structured as sole proprietors, S corporations and partnerships can deduct up to 20 percent of their qualified business income. But that percentage can be reduced after your taxable income reaches $157,500 (or $315,000 as a married couple filing jointly).

The amount of the reduction depends partly on the amount of wages paid and property acquired by your business during the year. Another complicating factor is that certain service industries including health, law, consulting, athletics, financial services and accounting are treated slightly differently.

The IRS is expected to issue more clarification on how these rules are applied, such as when your business is a mix of one of those service industries and some other kind of business.

- What are the new rules about

dependents and caregiving?

There are a few things that have changed regarding dependents and caregiving:

- Deductions.

Standard deductions are nearly doubled to $12,000 for single filers and

$24,000 for married joint filers. The code still says dependents can claim

a standard deduction limited to the greater of $1,050 or $350 plus

unearned income.

- Kiddie Tax.

Unearned income of children under age 19 (or 24 for full-time students)

above a threshold of $2,100 is now taxed at a special.

- Family credit. If

you have dependents who aren’t children under age 17 (and thus eligible

for the Child Tax Credit), you can now claim $500 for each qualified

dependent member of your household for whom you provide more than half of

their financial support.

- Medical expenses. You

can now deduct medical expenses higher than 7.5 percent of your adjusted

gross income. You can claim this for medical expenses you pay for a

relative even if they aren’t a dependent (i.e., they live outside your

household) as long as you provide more than half of their financial

support.

Stay tuned for more guidance from the IRS on the new tax laws, and reach out if you’d like to set up a tax planning consultation for your 2018 tax year.

Audit Rates Decline for 6th Year In a Row

(but don't get complacent)

IRS audit rates declined last year for the sixth year in a row and are at their lowest level since 2002, the agency reported. That's good news for people who don't like to be audited (which is everybody)!

But don't get complacent. A closer look at the IRS data reveals some audit pitfalls to beware. Here is what you need to know:

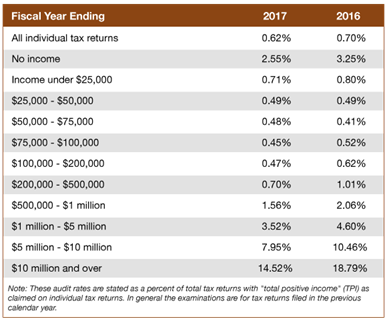

Audit rate statistics for individuals

Observations

- Low statistics for

audit examinations obscure the reality that you may still have to deal

with issues caught by the IRS's automated computer systems. These could be

math or typo errors or missing forms. While not as daunting as a full

audit, you need to keep your records handy to address any problems.

- Average rates are

declining, but audit chances are still high on both ends of the income

range: no-income and high-income taxpayers.

- No-income taxpayers are

targets for audits because the IRS is cracking down on fraud in refundable

credits designed to help those with low income, such as the Earned Income

Tax Credit (EITC). The EITC can refund back more than a low-income

taxpayer paid in, so scammers attempt to collect these refund credits

through fraudulent returns.

- High-income taxpayers have

increasingly been a target for IRS audits. Not only do wealthy taxpayers

tend to have more complicated tax returns, but the vast majority of

federal income tax revenue comes from wealthy taxpayers. Based on the

statistics, the very highest income taxpayers can assume they will be

audited about every six years.

- Complicated returns are

more likely to be audited. Returns with large charitable deductions,

withdrawals from retirement accounts or education savings plans, and small

business expenses and deductions are reportedly more likely to be the

subject of an audit.

Stay prepared

Though audit rates are declining, don't discount the possibility that you may still be selected randomly for an audit. Always retain your tax records and support documents for as long as you need them to substantiate claims on a return. The IRS normally has a window of three years from the filing date to audit a return, but this can be extended if the agency believes there's any fraudulent activity going on.

If you do receive an audit letter from the IRS, it's best to reach out for some professional assistance as soon as possible.

How to Handle a Gap in Health Care Coverage

Health care coverage gaps happen. Whether because of job loss or an extended sabbatical between gigs, you may find yourself without health care for a period. Here are some tax consequences you should know about, as well as tips to fix a coverage gap.

Coverage gap tax issues

You will have to pay a penalty in 2018 if you don’t have health care coverage for three consecutive months or more. Last year the annual penalty was equal to 2.5 percent of your household income, or $695 per adult (and $347.50 per child), whichever was higher. The 2018 amounts will be slightly higher to adjust for inflation.

Example: Susan lost her job-based health insurance on Dec. 31, 2016, and applied for a plan through her state’s insurance marketplace program on Feb. 15, 2017, which went into effect on April 1, 2017. Because she was without coverage for three months, she owes a fourth of the penalty on her 2017 tax return (three of 12 months uncovered, or 1/4 of the year).

While the penalty is still in place for tax years 2018 and earlier, it is eliminated starting in the 2019 tax year by the Tax Cuts and Jobs Act.

Three ways to handle a gap

There are three main ways to handle a gap in health care coverage:

- COBRA. If

you’re in a coverage gap because you’ve left a job, you may be able to

keep your previous employer’s health care coverage for up to 18 months

through the federal COBRA program. One downside to this is that you’ll have

to pay the full premium yourself (it’s typically split between you and

your employer while you are employed), plus a potential administrative

fee.

- Marketplace. You

can enroll in an insurance marketplace health care plan through

Healthcare.gov or your state’s portal. Typically

you can only sign up for or change a Marketplace plan once a year, but you

can qualify for a 60-day special enrollment period after you’ve had a

major life event, such as losing a job, moving to a new home or getting

married.

- Applying for an exemption. If

you are without health care coverage for an extended period, you may still

avoid paying the penalty by qualifying for an exemption. Valid exemptions

include unaffordability (you must prove the cheapest health insurance plan

costs more than 8.16 percent of your household income), income below the

tax filing threshold (which was $10,400 for single filers below age 65 in

2017), ability to demonstrate certain financial hardships, or membership

in certain tribal groups or religious associations.

Managing Money Tips For Couples

Spring is here and love is in the air. Or, it is as long as you aren't arguing over money with your special someone. Couples consistently report finances as the leading cause of stress in their relationship. Here are a few tips to avoid conflict over finances with your long-term partner or spouse:

- Be transparent. Be

honest with each other about your financial status. As you enter a

committed relationship, each partner should learn about the status of the

other person's debts, income and assets. Any surprises down the road may

feel like dishonesty and lead to conflict.

- Discuss future plans often. The

closer you are with your partner, the more you'll want to know about his

or her future plans. Kids, planned career changes, world travel, hobbies,

retirement expectations – all of these will depend upon money and shared

resources. So, discuss these plans and create the financial roadmap to go

with them. Remember that people in a long-term marriage may be caught

unaware if they haven't talked about the future and find out their

spouse's priorities have changed over time.

- Know your comfort levels. As

you discuss your future plans, bring up hypotheticals: How much debt is

too much? What level of spending versus savings is acceptable? How much

would you spend on a car, home or vacation? You may be surprised to learn

that your assumptions about these things fall outside your partner's comfort

zone.

- Divide responsibilities;

combine forces. Try to divide financial tasks

such as paying certain bills, updating a budget, contributing to savings

and making appointments with tax and financial advisors. Then periodically

trade responsibilities over time. Even if one person tends to be better at

numbers, it's best to have both members participating. By having a hand in

budgeting, planning and spending decisions, you will be constantly

reminded how what you are doing financially contributes to the strength of

your relationship.

- Learn to love compromise. No

two people have the same priorities or personalities, so differences of

opinion are going to happen. One person may want to spend, while the other

wants to save. Vacation may be on your spouse's mind, while you want to

put money aside for a new car. By acknowledging these differences of

opinion will happen, you'll be less frustrated when they do. Treat any

problems as opportunities to negotiate and compromise. Instead of looking

at the outcome as "I didn't get everything I wanted to do,"

think of it as "I sacrificed some of what I wanted out of love for my

partner and he/she did the same for me."

Securities and advisory services offered through LPL Financial, a

Registered Investment Advisor, Member FINRA/SIPC. Janell Israel &

Associates is not an affiliate company of LPL Financial.

The opinions voiced in this material are for general information only and are

not intended to provide specific advice or recommendations for any

individual.

This information is not intended to be a substitute for specific individualized

tax advice. We suggest that you discuss your specific tax issues with a

qualified tax advisor.

******************************************************************

All information is believed to be from

reliable sources, however we make no representation as to its

completeness or accuracy. The information contained in this newsletter is

provided by Mostad & Christensen, Inc.

The information is of a general nature and should not be acted upon in your

specific situation without further details and/or professional assistance. For

more information on anything in this newsletter, or for assistance with any of

your tax, business or financial strategy concerns, contact our

office.

This

message and any attachments contain information which may be confidential

and/or privileged and is intended for use only by the addressee(s) named on

this transmission. If you are not the intended recipient, or the employee or

agent responsible for delivering the message to the intended recipient, you are

notified that any review, copying, distribution or use of this transmission is

strictly prohibited. If you have received this transmission in error, please (i) notify the sender immediately

by e-mail or by telephone and (ii) destroy all copies of this message. If you

do not wish to receive marketing e-mails from this sender, please send an

e-mail reply or a postcard to 1585Kapiolani Blvd., Suite 1604,Honolulu, Hawaii 96814.

Please visit www.janellisrael.com for up-to-date financial information.